The journalist and secretary general of the National Union of Tunisian Journalists (SNJT), Fahem Boukadous, expressed, Wednesday December 24, 2025, his concerns about an amendment contained in the Finance Law for 2026, which, according to him, could weaken the foundations of the social state in Tunisia. In a post published the same day on his Facebook page, Mr. Boukadous analyzed in a technical and detailed manner the implications of the modification made to article 13 bis of the Value Added Tax Code.

A silent reform but with serious consequences

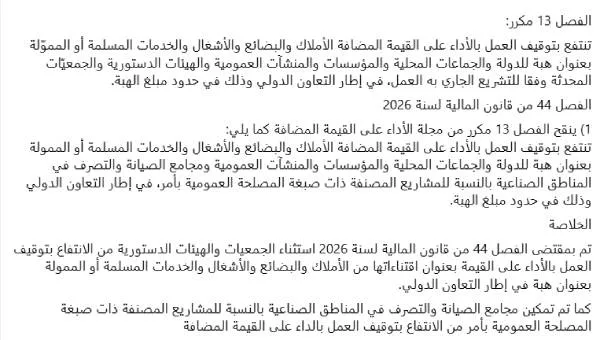

The heart of the reform lies in article 44 of the 2026 Finance Law, which modifies article 13 bis of the Value Added Tax Code. This article initially provides that “ benefit from the suspension of value added tax on goods, merchandise, works and services delivered as a donation within the framework of international cooperation, to the State, local public authorities, public establishments and associations created in accordance with the legislation in force “. This measure aimed to ensure that international donations intended for associations or non-profit structures were not subject to VAT, thus allowing their social and developmental impact to be maximized.

However, the amendment introduced by article 44 of the 2026 Finance Law now explicitly excludes associations and constitutional bodies from this system, while extending certain advantages to “ maintenance and management companies in industrial zones » for projects classified as being of public interest by decree.

« It’s not a simple technical adjustment », underlines Mr. Boukadous. “ This is a profound turning point in the philosophy of the country’s fiscal and social policy. Associations find themselves subject to tax costs which significantly reduce the real value of international funding and limit their capacity for action.. »

Concrete effects for associations and social development

According to Mr. Boukadous’ analysis, the suspension of VAT in the context of international donations is an essential mechanism to protect non-profit structures: unlike associations, community businesses continue to benefit from tax exemptions and facilities, which transforms VAT into a fixed cost for non-profit actors. The imposition of VAT on international donations will therefore result in:

- Reducing the size and scope of funded projects,

- A reduction in the number of beneficiaries of social or humanitarian actions,

- An increase in the complexity of administrative procedures and control, particularly for donations already made before the entry into force of the amendment.

« This change also creates major legal uncertainty “, warns Mr. Boukadous, “ with the risk of conflicts of interpretation or renegotiation with international donors, which could harm the credibility of the State and its ability to honor its commitments. »

A questioning of tax justice and the social state

The exclusion of associations illustrates a distortion of the principle of fiscal justice: community businesses continue to benefit from tax exemptions and facilities, while non-profit actors are imposed a fixed cost, with no tangible compensation for the public treasury.

« This reform forcibly shifts resources from the social field to taxation, which goes against the logic of financial efficiency and solidarity. », Explains the journalist. In the longer term, it risks weakening one of the practical pillars of the social state in Tunisia, by limiting the indirect support that associations can provide to social cohesion and the reduction of inequalities.

A silent but significant reform

Fahem Boukadous insists that the text was adopted without significant public debate. “ Silent measures have cumulative effects “, he warns, “ and this change, if not corrected, could gradually empty the very concept of a social state of its financial and practical substance. »

In summary, the Finance Law for 2026, through article 44:

- Excludes associations and constitutional bodies from the suspension of VAT on international donations,

- Extends the benefit of the suspension to industrial companies for projects of public interest,

- Reduces the effectiveness of international financing intended for social development,

- Creates a fiscal imbalance between community businesses and social actors,

- Threatens the legal stability and credibility of the State with international donors.

This analysis by Fahem Boukadous highlights a reform which, behind its technical appearance, could have profound consequences on the social mission of the State and on the role of the associative sector in Tunisia.

I.N.